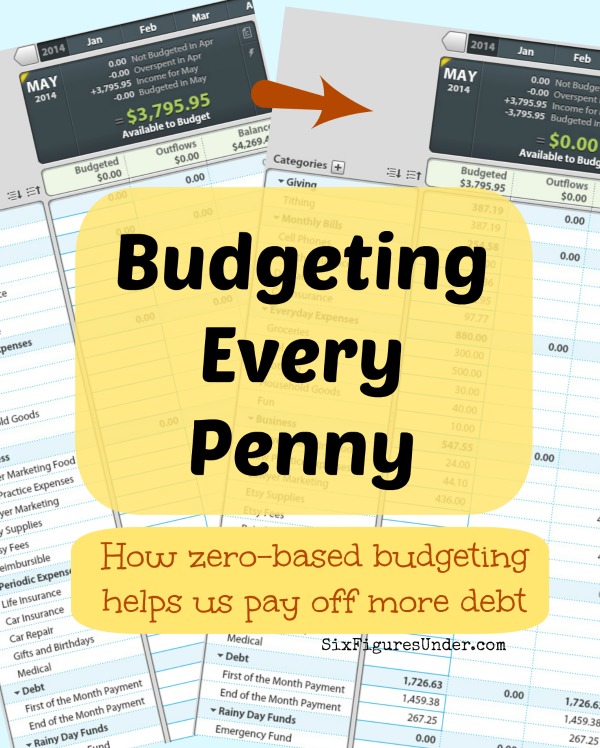

One of the problems with our previous budget was the inability to budget down to zero. We had categories with a set amount to spend, but there wasn’t a good way to deal with being over-budget or under-budget in a category and we were never quite sure how much we had leftover that we could put toward debt. I am in love with the way we are able to give every dollar a job now and put the maximum amount toward our student loan debt.

I want to show you how our we budget every penny at the beginning of the month and how it works for us. I will walk you through how we budgeted (our actual budget) for May.

Background

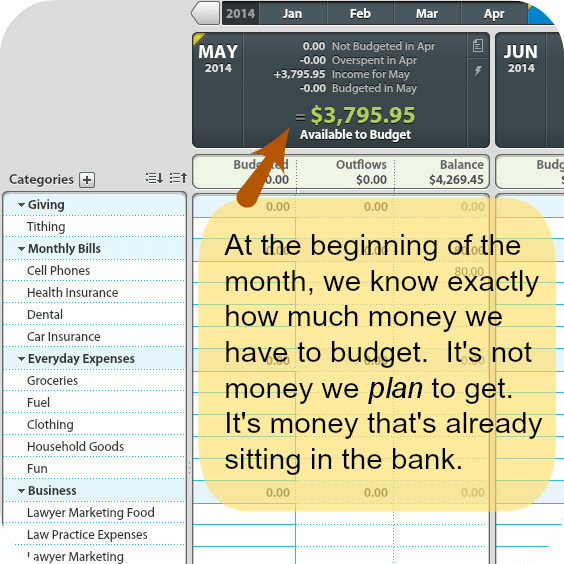

We are “living on last month’s income,” which means that when paychecks and other income come in during the month, we earmark it to be used the following month. Then, at the beginning of the new month, we know exactly how much money we have to work with that month.

In order to live on last month’s income, you will need a buffer of a month’s-worth of expenses. It may take several months of saving or using your tax return or other chunk of money to get into a position to live on last month’s income. It is worth every effort! There is so much peace of mind that comes when you aren’t living paycheck to paycheck, making sure to time the credit card payments just right so that nothing bounces.

Update: I have since written a detailed explanation on how and why we live on last month’s income.

Beginning of the Month

At the start of May, we had $3,795.95 to budget, which was all of our income during the month of April. Our ready-to-budget income is slightly higher than what I reported as our earnings during April. When I calculate and report our earnings each month, I report the net income from online sales (fees and shipping taken out), but the ready-to-budget income for the month includes payments I receive from Etsy and Ebay, before fees and/or shipping are taken out of them, since fees and shipping are one of the budgeted categories.

Allotting Money to Categories

This is the fun budget-y part! We go through the categories, starting with the most important ones.

- Tithing–

In May, we pay tithing of 10% of what we earned in April. We have always paid tithing, but we’ve scheduled it differently in the past. With the way we do it now, we know exactly how much it will be since we pay on last month’s income, so there isn’t any guessing.

- Fixed Monthly Bills–

These are bills that have the same amount due each month. They require no guesswork. For us, health insurance, car insurance, cell phone, and our dental discount plan all fall into this category.

- Everyday Expenses-

These are the categories where most of the action happens during the month. The categories we use are gas, groceries, clothing, household, and fun.

- Business Expenses–

Someday, we might have our own business budgets, but for now they are a part of our family budget. Our business categories include various category types.

- Some of these are fixed–For example, the law practice expense of $44.10 each month for law practice management software is the same each month.

- Some are variable but known— I know at the beginning of the month what I will owe in Etsy fees since my Etsy bill is calculated on the previous month’s sales and postage I purchased through Etsy.

- Some are very variable–For example we budgeted a guesstimate under Lawyer Marketing because my husband is hosting a seminar and we aren’t sure what the total cost will be. Other months, this category just includes a print ad.

- Some are just their own thing— Since my husband often makes purchases for work or scouts or church that he is reimbursed for, I keep a category to track those purchases. It should zero out by the end of the month.

- Periodic Expenses-

We think through the month and budget forany periodic expenses that are coming up that month, like car registration renewal, life insurance premiums, birthdays, medical bills, or car repair. If we weren’t in a total debt repayment mode, most of these would be sink funds, where we would allot a certain amount to them each month so that when the planned periodic bill came up the money would all be there ready to go.

You’ll notice that there are no credit card bills on my list. Once you get going on YNAB you don’t have to worry about where the money is going to come from to pay your current credit card bills because all the purchases made on your credit card are accounted for in your categories. The money to pay the bills is just chilling in our checking account. I don’t worry about it accidentally getting spent because we always spend according to our categories in YNAB (not the balance of the checking account).

When you start YNAB, your credit cards will each have their own category (called “pre-YNAB debt) until you pay off the balance that was already on the card. New purchases after starting YNAB will not add to that credit card category because they are accounted for in their actual category like “clothing” or “groceries.”

Allotting Money to Debt

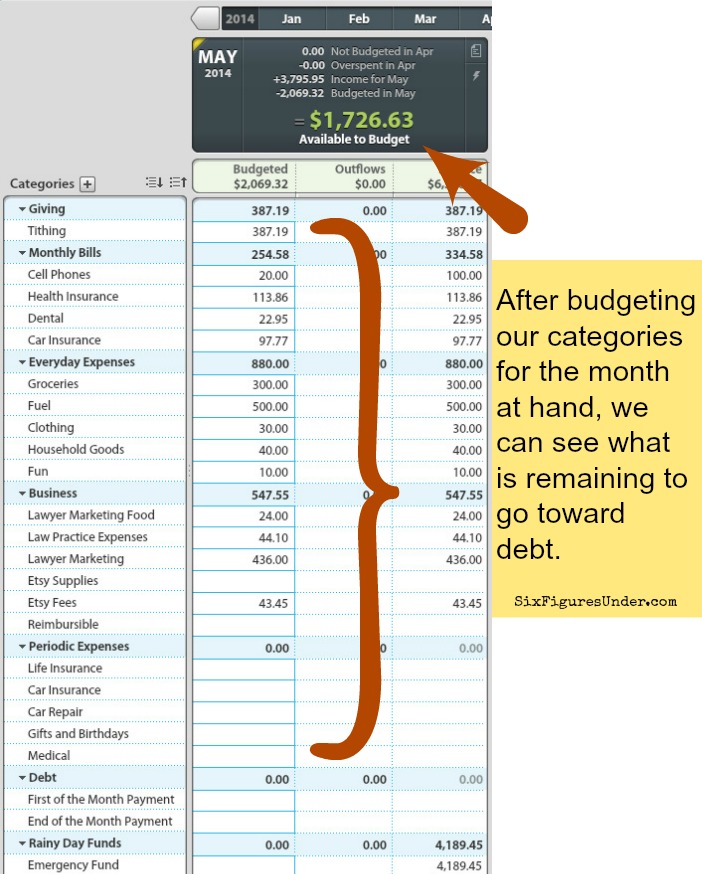

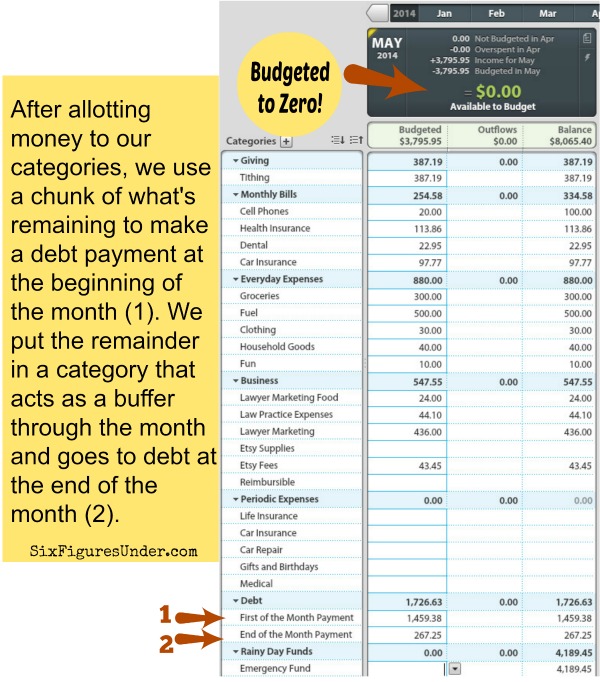

After allotting money to all our categories in May, we had $1,726.63 that we could potentially put toward debt in May. We didn’t want to pay every last penny on the first of the month though, because there are still thirty more days where unexpected expenses could pop up.

We like to pay a big lump toward debt at the beginning of the month,but leave another chunk in a holding tank category until the end of the month. Usually we pay a round-ish number, but we were pretty close to getting one of our debts paid off, so our debt payment at the beginning of May was $1,459.38. The remaining $267.25 is in our hold tank creatively titled “End of the Month Payment.”

When we go over budget on a category (accidentally or intentionally), our first line of defense is to adjust the budget in other categories. For example, if it looks like we are going to be over on gas, I will subtract from our clothing budget and add it to the gas budget. If an unexpected expense comes up (like bad news at my dentist appointment this month), then I will have to get the funds from the “End of the Month Payment” category. Anything beyond that will be taken from the Emergency Fund (and later repaid).

A few notes on debt: We are in an unusual position right now that we don’t have any minimum payments due. If you have minimum payments, make sure that you are paying at least the minimum due on those. That should be high in the priority list when allotting your money into categories. If you have multiple debts, they should each have their own category. Since all of our debt is student loans, we keep the debt category to just these two categories.

At the End of the Month

At the end of the month, there is usually some money remaining in the “everyday expenses” categories since we don’t spend exactly $300 on groceries or exactly $500 on gas. I add whatever is remaining in each category at the end of the month to the “End of the Month Payment” category. When the balance of each category is zero, I make a debt payment for the amount of the “End of the Month Payment” category.

Update: I have since written a detailed post about this: Maximizing Our Debt Repayment at the End of the Month

The exception is the cell phone category. Instead of sending my dad a check for $20 each month, I let that category accumulate for a while before I send a check. This month it will be up to $100, so I will probably send off a check. If I weren’t trying to get every possible penny put toward debt, I could let the extra money in a category “roll” into the next month’s budget.

You can do it too!

You don’t have to have YNAB’s software to make a budget like this work, though it is convenient and motivating. You could set up something on your own if you like. It’s no secret that I am a do-it-yourself penny pincher, but even so YNAB has been worth every penny. You can try it free for 34 days. Be sure to check out YNAB’s amazing live online classes so you can make the most of your trial.

However you do it, budgeting down to zero can have amazing results. Zero-based budgeting will let you take charge of exactly where each dollar goes, so not a single dollar disappears. Have you noticed how they tend to disappear if you don’t watch them closely?

Right now and for as long as we can remember we’ve lived paycheck to paycheck-Setting “budgets” based on what we expect we might get paid. Living off last months income would be a dream, but we can never seem to get ahead enough to even make that a reality. How do you get in a position where you’re able to live off last months income and actually budget off of what you already have, not what you project to receive?

I know this question is a few years old, but for those who just found this post, here is my experience so far. One of the YNAB concept is the “Age of Money”: How old is the money that you are spending right now? Getting that to 30 days or more sounded like a pipe dream.

I’ve been using traditional budget tools like spreadsheets and Mint but always felt that I was living paycheck to paycheck and my credit card balances seem to never decrease. I started YNAB with 1 day age which means I’m spending the money as soon as I make it. Within days, YNAB was forcing me into a habit of rethinking my each of my spending decisions and only spending the money I have budgeted. I knew exactly where every one of dollars is going. After that I noticed that I was actually able to put away a little bit more into savings. And watching the “Age of Money” number go up, slowly but surely, reinforced my resolve to stick to my budget.

Then one day when I finished budgeting for the current month, I had money left over in “To be Budgeted”. I had to double take all my categories because I thought I must have missed something. Nope. Every single category was given the proper budget. That money going into the next month’s budget. Just enough to partially budget one category but it was a revelation. It motivated me that it was working.

It took a few months but I am now spending from the previous paycheck. Even that is a huge relief in my daily life because I’m not thinking about my next paycheck as much.

YNAB is such a simple concept and I can’t believe I hadn’t found it sooner. After the initial trial period, I had to “scrape the barrel” to find the money to pay for the subscription but it was worth every penny.

Hi Stephanie!

I appreciate this page (it answered why to budget to 0. I knew Dave Ramsey said to, but couldn’t remember why.) I like that you tithe! Are you a Christian?

–when prefer to be used zero budget??

My wife, Heather is the budget maker and I am the spender in the family. It has been hard finding a system that works for irregular income (tips, side jobs etc.). I have been telling everyone about this. It is awesome, thank you!

Stephanie, thanks for all your great information. I tried YNAB a few months ago and didn’t stick with it. I think I made it too complicated and then went back to Mint. The problem with Mint is there is not much interaction with it to save money. Any suggestions?

That 10% you spend on ‘tithing’ every month (also known as cult dues) could be much better spend ACTUALLY PAYING DOWN THAT 80 GRAND OF DEBT YOU STILL HAVE. Why on earth anyone would willingly choose to give 10% of their entire earnings to some feel-good-club that provides nothing in return for you other than fake warm and fuzzy feelings you could just as easily get from having your debt paid down sooner.

I’m sure your ‘god’ will forgive you for not paying tithing for as long as it takes you to get out of debt. If the people that hold student loan debts have a mechanism for allowing for economic hardship and low-income, then I bet your all-forgiving ‘god’ won’t have a problem with you putting your tithing towards paying down debt.

Or you could continue to throw away hundreds of dollars a month on your cult membership. Either way, I immediately stopped reading your blog as soon as I saw that you pay 10% tithing while you’re ‘six figures under’ (might as well still be six figures under at 80 grand of debt).

Thanks for sharing your opinion. You aren’t the first person to voice this concern. You might be surprised that I totally see where you’re coming from. If I didn’t believe what I believe I would think it was crazy too! For example, drinking, smoking, and tattoos are all things that I don’t “believe” in, so to me it is crazy that people spend their money on those thing. At the same time, I understand that we all put our money where are priorities are. We all have different priorities. And that’s just fine!

Tithing works for me. Other things work for other people. I don’t expect people to agree with me, but for anyone who is curious about my perspective on why we do the tithing thing even though we’re in debt, I wrote about it here.

Stephanie,

Nice response to that…. Positivity is always the best way to handle things and people.😊

Class act! Brava!

The name of your blog made me smile. Thanks for explaining a new way of looking at finances. Pinned to my “Frugal Family Fun” board.

Thanks Suzanne! 🙂

You can also get the YNAB for free if you’re a student. I was able to get mine for free.

I love the idea that the money’s already in the bank so there are no surprises during the month. That must really help you sleep. I’m sure building up that buffer takes some effort, but it really sounds worth it.

It is very comforting to have that buffer there. It’s definitely worth the effort!

Since you aren’t allocating money to your periodic bill categories what do you do when they come up? How are you planning for them? Do you just have a smaller debt payment for the month one or more of them comes up? We just started using YNAB and love it! We currently are also in “debt pay off” mode. I do allocate funds to our periodic bills but doing so does subtract from our debt snowball. Just wondering how you handle it! Thanks!

Hi Kristin! We just have a smaller debt payment on the months when periodic expenses come up. At the beginning of the month that they are due, I budget them in. This month, we have a car registration due (and it needs a SMOG test too), so I put $200 in the car registration category. This works well for us because we have no minimum payments due on our student loans (thanks to IBR), so we can be more flexible.

I have just upgraded from the trial and purchased YNAB this May. The improvement in my finances has been almost instantaneous! Just moving from keeping track of my balances in YNAB instead of looking at my bank balance has made a huge difference (currently have $1100 sitting in my checking, all with jobs but haven’t been tempted to spend it!).

One question: I see that you have a ‘debt’ category – does that mean that you don’t have your student loans on budget? I have a car loan and master card on budget that I am paying down, but I hate looking at them in the red each time I log in. I’m considering putting the loan as off-budget but I guess I need to keep my credit card on, in case I spend from it….

Can’t wait till I’m out of the red! But with YNAB it seems closer than before.

I’m glad you’re loving YNAB too Kelly!!

When we started, we had the Pre-YNAB debt category like everyone does who uses a credit card (since there is always spending from the month before you started YNAB that is on your credit cards). We didn’t put our student loans into YNAB. Instead we have a category in our budget (2 actually) where we budget the money we will put toward our loans. When we paid off all of our pre-YNAB debt we hid those categories since we didn’t need them anymore because all future spending on the credit cards would be accounted for in the categories.

In your case, I think it would be fine to make your loan off-budget and keep the credit card on-budget. The difference being (like you noted) you could spend from the credit card, but wouldn’t spend from the loan (though it still accrues interest). Just make sure you have a debt category where you budget your payments (like you would a rent or mortgage payment).

Best wishes for a quick debt repayment!! 🙂

Pretty good looking program but I noticed you omitted any type of housing payments. Did you omit these intentionally? Or do you own a home and this is included in your debt? Just curious as our rental cost takes up about 85% of our monthly income :/ but our debt makes it impossible to buy a home. Wanna get an idea if this system would help us. Thanks! Good post 🙂

Hi Ami! We have an unusual situation right now. We live in my in-laws’ basement. We turned it into a little apartment (2 bedrooms, 1 bath, a kitchen and living room). It was their idea to let us live here while we pay off our law school debt.

As far as YNAB goes, you would have your rent, utilities, and other costs in their own categories and things would work the same. Our budget just looks simplified because our expenses are really minimal right now (which is a huge blessing). That is our real budget. At the end of the month (in addition to our regular monthly debt repayment update with all our numbers) I will show (with more screenshots) how we take the money left and put it toward debt.

Wow! 85% of your income is a lot to pay for rent! Does that include utilities? That sounds painful!

Thanks for sharing and linking up with us at the #WWDParty!

I definitely want to do this. Living off last month’s income would GREATLY improve financial peace of mind. Thanks for the idea!

It really is wonderful and brings so much peace.

Interesting post! I’ve tried so many programs, I’m afraid to throw in any more money, cause I can’t seem to stick to them. But it’s great to read how someone actually works with it. You explain it very clearly and I will bookmarking this post to be able to come back to it. Thanks!

Elivra, I was the same way, well not that I had spent a lot of money in the past, just that I’m leery of spending money on something I could do myself with a spreadsheet. Before I bought YNAB, I signed up for their 9 day email intro series, and watched 3 of the hour-long online classes. By the time I put the money down, I knew how to use the program, was motivated and excited to use it. I even got a glimpse of how it would save us money. It’s actually helping us even more that I expected, which is pretty amazing!

Great post. We are struggling with trying to get things under control and live within the budget. This blog will be a great resource.

Thanks Laina. Good for you for working to get your budget in order!

How much does YNAB cost? I know that you can get a free 34 day trial but I’m curious to know how much it will cost after that time is up. My husband has student loans coming up and the thought is stressing me out because it’s about $80,000.

YNAB’s regular price is $60, but you can get $6 off through my referral link.

It is amazing how fast those student loans add up (and grow)! When my husband finished his JD/MBA (law and business degrees) we had over $130,000 (and we lived frugally!), so I totally know what you mean. 🙂

We are committed to our Excel spreadsheet and loving it. Also working on living off of last month’s income. That alone will be a huge step in the way of financial peace. 🙂

Yes Laurie! It is huge and makes such a difference!

Is that a particular program that you are using for budgeting?

Yes Tieranie. It’s YouNeedABudget, but everyone calls it YNAB (pronounced “why nab”). It’s AMAZING! I wrote more about it here.

I’ve used YNAB for 3 years now and love both the software (very easy to use) and the zero budget concept.

I have subcategories set up for those items that are tax deductible (we have a small farm business) like travel expenses, chemicals, tractor fuel, etc. This makes it a little easier at tax time.

I also make use of the memo tags for the months payments. As an example I have a subcategory for home maintenance and repair and since it’s rarely used I put a note as to what was done and itemize the cost. This removes any guessing as to what the heck was done several months down the road. I actually use the memos for the clothing category so I know exactly what was bought. This helps to curb unnecessary spending.

Anyone looking for a way to track, monitor, and budget their spending should definitely give YNAB a try!

Thanks for sharing Tricia! That’s a great idea to keep track of the tax deductible business expenses like that!

I use the memos too! I love that you just have to hover over them to see the memo (instead of click through a couple screens).

I have heard so many great things about YNAB. The biggest thing holding me back is that my computer is on its last legs and we’re planning on upgrading this month. (Seriously, this computer literally has holes in it and the most recent power cable is showing its wires) What’s the point in downloading new software when you’re just going to get a new machine, right? I’ll definitely be sending your post to my husband so he can get an idea of zero-base budgeting. And I really like how you use the previous month’s income, that makes it so much cleaner than having to guess at the upcoming income.

Hooray for getting a new computer soon! It sounds like you’ve gotten your money’s worth out of your current one! 🙂

It is so nice to know exactly what we have available to spend. We use credit cards for everyday purchases and pay them off each month and it’s really nice to know that there is always money in our checking account to pay the bills. YNAB has really great free online classes that help a ton!

I prefer not to “hold back” any debt payment just-in-case, because I’m horrible at defining emergency vs “I want that”. What we do is have a separate line item for “emergency”. It has a set amount in it’s balance, if a true emergency does come up, we budget it negatively (take money out of that bucket) and put it where we need it. Then the next month, we fill that back up before we allocate the rest of our income.

That makes sense. You know yourself best!

We are pretty careful about touching the emergency fund and the end of month debt payment, so I know they won’t be used unless it’s completely necessary. We’ll pull from other categories first even though we don’t have a lot of fluff in our budget.

Your business expenses should be kept in a separate account and you pay yourself out of that account,

you’re going to get in trouble with the IRS.

Also, I would recommend getting rid of CCs altogether my wife and I held out against Dave Ramsey’s advice for a while to get “rewards” but have since decided it’s not worth it…based on the risk associated with them granted it is extremely low base so on our position but the risk isn’t still present.

Thanks for the advice on YNAB!